- India introduces new tax amendments to classify cryptocurrencies as Virtual Digital Assets, requiring traders to disclose previously undisclosed crypto gains.

- Traders may face a 70% penalty on undisclosed crypto profits, with the amendment set to apply retrospectively starting February 1, 2025.

India's Finance Minister Nirmala Sitharaman, in her Union Budget 2025 announcement, outlined new amendments to the country's tax laws that could significantly affect cryptocurrency traders.

Cryptocurrencies will now be classified under Section 158B of the Income Tax Act, which governs the reporting of undisclosed income.

As a result of this change, cryptocurrency gains will face block assessments if not properly disclosed, aligning them with traditional assets such as money, jewelry, and bullion in terms of tax treatment.

The amendments redefine cryptocurrencies as Virtual Digital Assets (VDAs) under the tax code, marking a significant shift in the regulation of digital assets in the country.

According to the new provisions:

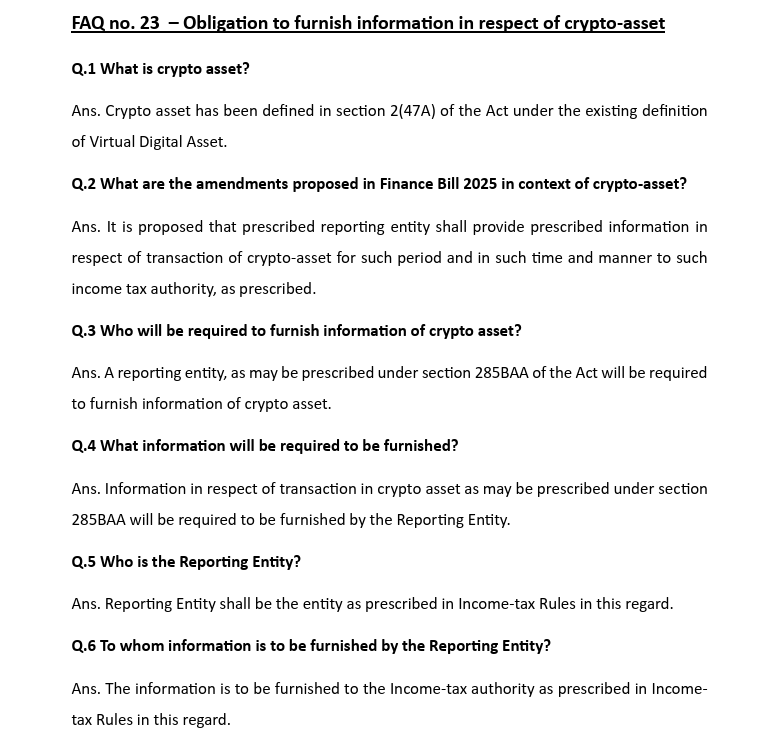

“Crypto asset has been defined in section 2(47A) of the Act under the existing definition of Virtual Digital Asset[…] A reporting entity, as may be prescribed under section 285BAA of the Act, will be required to furnish information of crypto asset.”

The amendment will take effect on February 1, 2025, and applies retrospectively, meaning traders will need to account for previously undisclosed gains.

This move follows recent reports indicating substantial tax gaps in the cryptocurrency sector. In December 2024, India’s Minister of State for Finance, Pankaj Chaudhary, revealed that the government had uncovered 824 crore Indian rupees ($97 million) in unpaid goods and services taxes (GST) from various crypto exchanges. This came months after law enforcement agencies demanded $85 million in unpaid taxes from Binance.

Under the new tax framework, traders who fail to report their crypto gains could face severe penalties. A tax penalty of up to 70% could be levied on previously undisclosed profits if they are reported more than 48 months after the relevant tax assessment year.

The updated provisions read:

“70% of the aggregate of tax and interest payable on additional income disclosed in the updated income tax return [ITR].”

This amendment follows regulatory actions against crypto exchanges operating in India, with Bybit suspending its services in January 2025 due to increasing regulatory pressure. Meanwhile, global attention on crypto tax laws is rising, with the US IRS implementing similar measures starting in 2025, requiring centralized exchanges to report crypto transactions for tax purposes.

Edited by Harshajit Sarmah